- According to UK government figures, in the two years to March 2023 an average of 65% of households in England owned their own homes1, with roughly half of these people owning their home outright and half having a mortgage2.

- On a typical £200,000 mortgage with a 25-year term left, a simple calculation shows that a 0.9% mortgage rate hike increases the monthly interest paid by approximately £1503.

- We prefer to own industrial real estate which is often considered a superior investment to residential property because of longer lease terms, higher rental yields, and lower maintenance responsibilities.

Residential property tends to be the most widely held asset, and, given its physical nature and social acceptance, is often the easiest to understand. It is also typically the largest single purchase an individual will make in their lifetime. Overall, this means the property market gets significant coverage in the media as a litmus test for the economy, personal wealth and consumer sentiment.

Recently, Bloomberg and Nationwide Building Society reported that UK house prices fell at the fastest pace for almost a year, and that the average price of a home dropped by 0.6%

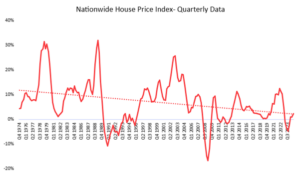

4. Nationwide publishes a quarterly house price growth figure that dates to 1974, presented in the chart below. The trend highlights a broad slowing of house price growth over the last five decades.

Source: Nationwide HPI News - Charts

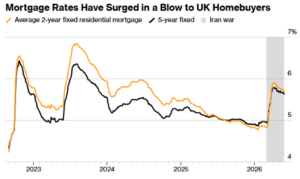

The recent fall is being attributed to the war in Iran, which has led to increased borrowing costs for consumers. The average two-year fixed-rate mortgage currently sits at 5.68%

5.

Source: Nationwide Reports First UK House Price Decline in Five Months - Bloomberg

Does it matter for the economy?

Housing investment is a small part of UK gross domestic product (GDP). Buying a newly-built home directly contributes to GDP through investment in land and materials as well as creating jobs in areas like law and estate agency. Employing over 12 million people, the property sector generates £1.7 billion annually

6 - less than 1% of UK GDP

7. However, this does not capture the second order effects.

Economic theory suggests when house prices go up, homeowners feel better off and more confident. Some people will borrow more against the value of their home, either to spend on goods and services, renovate their house, supplement their pension, or pay off other debt. The reverse is true when house prices fall. In reality, the effect on the economy is limited, relating more to sentiment than anything tangible.

Does it matter for me?

Individuals tend to change their spending habits to some extent, depending on how wealthy they feel overall. However, housing is illiquid and it is hard to capitalise efficiently on any increase in value.

For the cohort of individuals who own their homes outright, anaemic house price growth should be relatively inconsequential. For those in the process of selling a property, slower house price appreciation is likely to be broadly reflected across the market. As a result, whilst they may realise a lower sale price than would otherwise have been the case, the cost of purchasing a replacement property should also have risen by less, leaving their relative position largely unchanged.

For individuals who have a mortgage, the most important factor will be higher mortgage rates. Whilst rates on home loans have fallen from their recent highs, the average two-year fixed-rate mortgage is still at 5.68%. That’s almost 0.9% higher than in late February, just before the US and Israel bombed Iran

8. On a typical £200,000 mortgage with a 25-year term, a simple calculation shows that a 0.9% mortgage rate hike increases the monthly interest paid by approximately £150

9.

Bowmore portfolios

This is an opportune time to comment on the property market since the property investment trust we widely hold, Picton Property Income Ltd, is in the throes of being taken over by two competitors. Rather than residential property, it invests in commercial and industrial real estate. Industrial real estate is often considered a superior investment to residential property because of longer lease terms, higher rental yields, and lower maintenance responsibilities generally attracting stable tenants and fewer emotional disputes than residential housing

10.

Picton’s share price has been trading at a discount to the actual value of their property portfolio (NAV). The board of Picton identified this discount and effectively put the business up for sale in early 2026, hoping to close the gap between the NAV and the share price.

The sale review phase has attracted a joint bid from two investment trusts, Schroder Real Estate Investment Trust and LondonMetric Property Plc. The initial proposal is that Picton shareholders will receive shares in both investment trusts, reflecting an offer value of 78.2p per share. This offers a premium to the current share price; however, the offer implies a discount of around 9% to Picton’s NAV and denies investors a cash exit.

Should the deal be rejected by shareholders we would be happy holders of a well-run company and continue to collect a c.5% income yield per annum, in addition to some capital growth into the future.

Picton is held in Core, Income and ESG models.

Source: AlphaTerminal, data as at 10/06/2026

The value of your investments can go down as well as up, so you could get back less than you invested. Past performance is not a guide to future performance.

Sources:

1 Home ownership - GOV.UK Ethnicity facts and figures

2 How does the housing market affect the economy? | Bank of England

3 Bowmore Asset Management

4 Nationwide Reports First UK House Price Decline in Five Months - Bloomberg

5 Nationwide Reports First UK House Price Decline in Five Months - Bloomberg

6 Real estate article business.gov.uk international

7 IMF DataMapper

8 Nationwide Reports First UK House Price Decline in Five Months - Bloomberg

9 Bowmore Asset Management

10 Residential vs commercial properties: guide for landlords