Important information: The value of investments and any income derived from them may go down as well as up. You may not get back the amount originally invested. Past performance is not a reliable indicator of future results.

Key takeaways

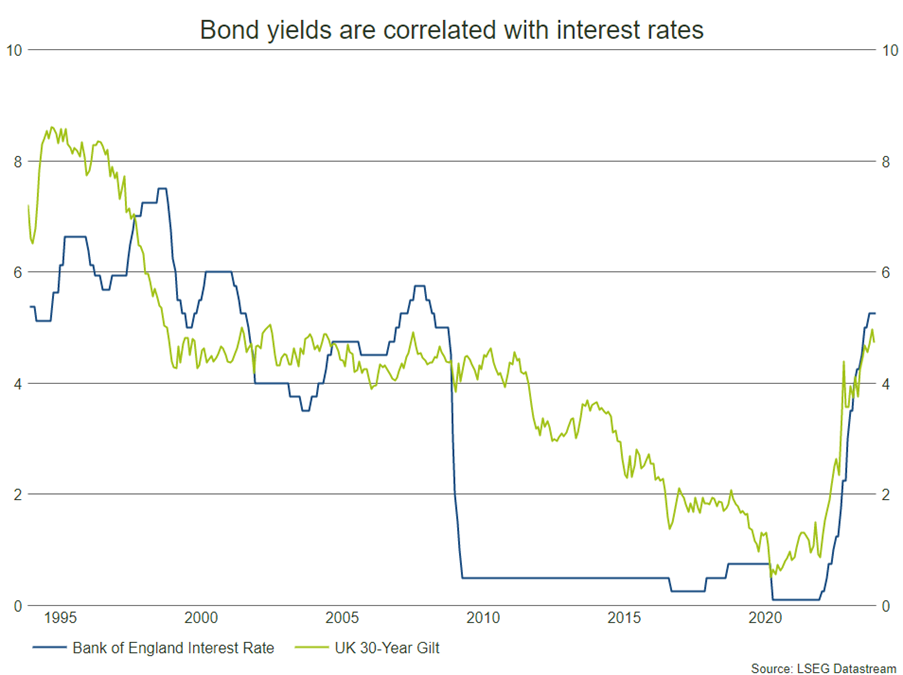

As we have written in past notes, rising interest rates over the last two years have had the opposite effect on bond prices, with values being pushed lower and yields ballooning to levels we have not seen in more than a decade. Thirty-year UK gilts have been yielding well over 4% since May, and at one point broke 5%. When yields rise prices fall, and this presents an opportunity for investors to buy into these markets at attractive points in anticipation of a pivot in monetary policy.

Bowmore portfolios

We have recently slightly increased our exposure to UK government bonds, bringing in a long-dated gilt that offers the upside potential described above. When interest rates are cut in the UK, longer-dated bond prices are positioned to rally. In the interim, buying in at a lower price means the income paid to investors represents a healthy yield. We have kept this allocation modest for now, as volatility in this sector tends to be higher due to interest rate sensitivity.

As we have written in past notes, rising interest rates over the last two years have had the opposite effect on bond prices, with values being pushed lower and yields ballooning to levels we have not seen in more than a decade. Thirty-year UK gilts have been yielding well over 4% since May, and at one point broke 5%. When yields rise prices fall, and this presents an opportunity for investors to buy into these markets at attractive points in anticipation of a pivot in monetary policy.

Bowmore portfolios

We have recently slightly increased our exposure to UK government bonds, bringing in a long-dated gilt that offers the upside potential described above. When interest rates are cut in the UK, longer-dated bond prices are positioned to rally. In the interim, buying in at a lower price means the income paid to investors represents a healthy yield. We have kept this allocation modest for now, as volatility in this sector tends to be higher due to interest rate sensitivity.

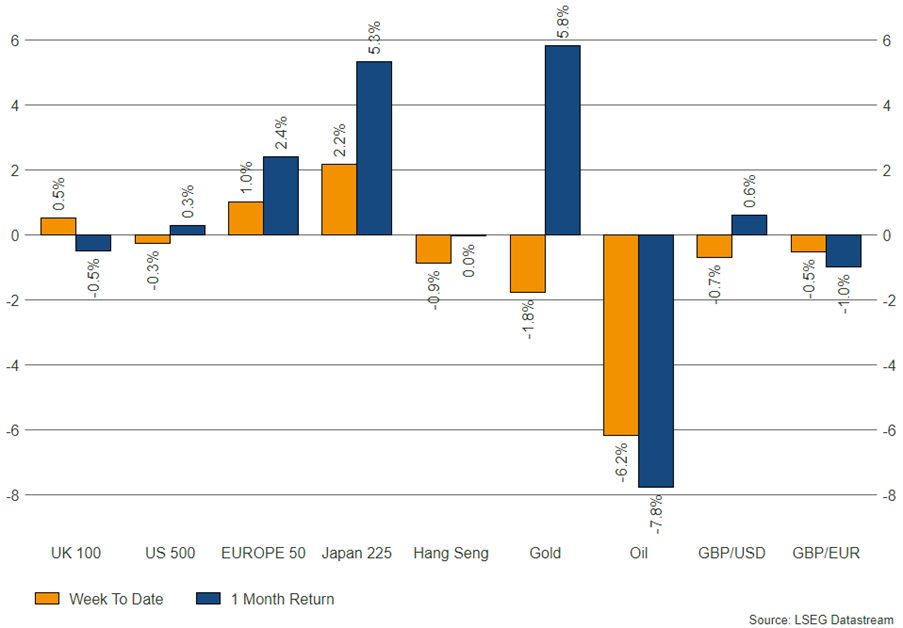

- Equity markets up 4.0% month-to-date on peak interest rate rhetoric.

- Bond prices at depressed levels due to tighter monetary policy over last two years.

- Attractive opportunity for longer-dated bonds to appreciate when rates are cut.

As we have written in past notes, rising interest rates over the last two years have had the opposite effect on bond prices, with values being pushed lower and yields ballooning to levels we have not seen in more than a decade. Thirty-year UK gilts have been yielding well over 4% since May, and at one point broke 5%. When yields rise prices fall, and this presents an opportunity for investors to buy into these markets at attractive points in anticipation of a pivot in monetary policy.

Bowmore portfolios

We have recently slightly increased our exposure to UK government bonds, bringing in a long-dated gilt that offers the upside potential described above. When interest rates are cut in the UK, longer-dated bond prices are positioned to rally. In the interim, buying in at a lower price means the income paid to investors represents a healthy yield. We have kept this allocation modest for now, as volatility in this sector tends to be higher due to interest rate sensitivity.