- 172 vessels have crossed through the Strait of Hormuz since the US and Iran signed a deal1

- At the time of writing, the oil price is at pre-conflict levels (Brent Crude $72.96 and West Texas Intermediate $69.82 a barrel) 2

- China imported 20% less oil in April compared to the year before4

As part of the 14-point US–Iran agreement to extend the ceasefire, the US Navy has begun lifting its blockade, along with removing any restrictions or impediments imposed on Iranian ports during the conflict. This has enabled maritime traffic through the Strait of Hormuz to resume.

However, ten days after the announcement, shipping volumes through the Strait are subdued, with approximately 40 vessels transiting per day compared with a pre-conflict average of around 140. Despite this, oil prices have fallen sharply, retracing much of their recent gains and moving back towards pre-conflict levels

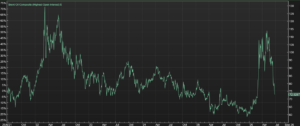

1. This week, we examine several factors behind the rapid decline in oil prices.

Brent Oil Composite over 5 years (highest open interest $)

Source: Alpha Terminal, 25/06/2026

China

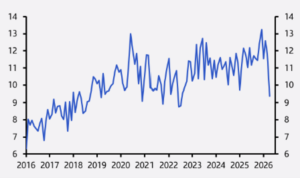

Chinese crude oil imports fell by a staggering 20% year-on-year in April, marking their sharpest decline since the pandemic. While China does not publish official data on its strategic petroleum reserve volume, most estimates suggest it has taken advantage of relatively low oil prices in recent years to build a stockpile of approximately 1.4 billion barrels

4. According to Graham Allison, a 1.4-billion-barrel reserve is enough to cover c.88 days of total consumption, or 127 days of the seaborne crude imports that come through chokepoints like the Strait of Hormuz

7.

That, together with the divergence between oil imports and seemingly stable domestic consumption suggests that China has been drawing down these inventories during the period of elevated prices in March, April and May

4. Stepping back, this strategic decision by the world's largest oil importer to utilise existing inventories, rather than continue its purchasing programme, was likely a significant factor in keeping oil prices below $100 per barrel for most of the conflict

3.

China Crude imports (million barrels per day)

Source: Capital Economics, 2026

Russia

Sanctions have been imposed on Russian oil and gas exports since its invasion of Ukraine in 2022 and have been progressively tightened over the past year, including measures targeting counterparties trading with Russia. These sanctions appeared to be having an effect, with Russian exports falling to their lowest levels since the start of the war, placing pressure on export revenues, government finances and, more broadly, the Russian economy

5.

However, Trump's decision to temporarily ease certain sanctions by allowing countries to purchase sanctioned Russian oil at sea provided Russia with a much-needed source of capital at a critical time

6. At the same time, the increase in available supply likely helped to moderate oil prices by easing the imbalance between global supply and demand.

OPEC

As we wrote about in May, the UAE’s decision to leave OPEC marked a major shift in oil market dynamics, with a removal of the regions 3 million barrel a day limit on production. At current capacity levels, the UAE are able to produce a further 1 million barrels of oil per day, increasing global supply by c.1%, and putting downwards pressure on price

4.

Bowmore portfolios

While direct commodities exposure isn’t an allocation within our managed portfolios, we do pay close attention to energy price levels given the direct impact a spike in prices can have on inflation. Further, as we have seen in recent months, a barrier to the free movement of energy causes a knock-on effect to the building blocks of the portfolio we manage, fixed income and equity.

We have taken the opportunity, recovering from the March sell off, to rotate exposure within the alternatives asset class, away from a market neutral hedge fund strategy towards infrastructure exposure, giving defensive core asset exposure for example to hospitals, schools and transport hubs as well inflation protection since rent reviews are tightly linked to RPI. Within core portfolios, we have introduced International Public Partnerships investment trust, which has returned 4.63% since purchase just 6 weeks ago. This short-term performance may not be indicative of longer-term returns and reflects a limited time period.

Source: Alpha Terminal, data as at 26/06/2026

The value of your investments can go down as well as up, so you could get back less than you invested. Past performance is not a guide to future performance.

Sources:

1 BBC, 2026

2 Alpha Terminal, 2026

3 Statistia, 2025

4 Capital Economics, 2025

5 Chatham House, 2026

6 Reuters, 2026

7 Graham Allison, 2026